What Happens to Your FEGLI Life Insurance When You Die? A Federal Employee’s Complete Guide

Most federal employees don’t spend much time thinking about life insurance. That’s understandable. Between work, family obligations, retirement planning, and the endless stream of decisions that come with everyday life, FEGLI tends to become one of those benefits that quietly exists in the background. You know you have it. You see the deduction on your paycheck. And you assume that if something ever happened to you, your family would be taken care of. But over the years, we’ve discovered something interesting when talking with federal employees.

Many know they have FEGLI. Few know how much they actually have. And almost nobody knows what really happens when a claim is filed. That uncertainty can create unnecessary stress during what would already be one of the most difficult times imaginable for a family.

Let’s change that.

In this guide, we’ll walk through exactly what happens when a federal employee covered by FEGLI passes away, how benefits are paid, how long the process typically takes, who receives the money, and why understanding these details today can help your family tomorrow.

Meet Mark

Let’s start with a hypothetical example.

Mark is a 54-year-old GS-14 employee with twenty-six years of federal service. Like many federal employees, he’s responsible, organized, and reasonably confident that his benefits are in good shape. He has FEGLI Basic coverage. He contributes to his TSP. He has a mortgage, a spouse, and a retirement plan that’s beginning to take shape. One evening, while discussing retirement with his wife, she asks a simple question:

“If something happened to you, what would I need to do?”

Mark pauses. He knows he has life insurance. But he doesn’t know:

- Who would contact the insurance company

- How much would actually be paid

- How long the process would take

- Whether the money would arrive as a check

- If the benefit would be enough

If you’re reading this article, there’s a good chance you’ve asked yourself some of those same questions.

Understanding What FEGLI Actually Provides

The Federal Employees’ Group Life Insurance program, commonly known as FEGLI, is the largest group life insurance program in the world. For many federal employees, FEGLI Basic coverage is the foundation of their family’s financial protection. The formula is surprisingly simple.

Basic FEGLI coverage equals: Your annual salary, rounded up to the next $1,000, plus an additional $2,000.

Let’s look at a real-world example.

Suppose Mark’s annual salary is $135,000. His salary is already an even thousand-dollar amount, so no rounding adjustment is necessary.

FEGLI would add the additional $2,000. That means Mark’s Basic FEGLI benefit would be approximately $137,000.

For some families, that sounds like a substantial amount of money. For others, especially those carrying a mortgage or relying heavily on one income, it may be far less than they expected. We’ll revisit that issue later. For now, it’s important to understand that FEGLI doesn’t automatically pay itself out. Someone must begin the process.

The First Thing Your Family Must Do

One of the most common misconceptions about life insurance is that insurance companies automatically know when someone passes away. That isn’t how the process works.

After a federal employee dies, a claim must be submitted. Typically, this responsibility falls to:

- A surviving spouse

- A designated beneficiary

- The executor of the estate

The claim process generally requires:

- A certified death certificate

- A completed FE-6 claim form

- Basic identifying information

Fortunately, funeral homes often help families obtain certified death certificates, which makes this step easier than many people expect. Still, it’s important that your loved ones know where to find your beneficiary information and basic employment records. A little organization today can save a tremendous amount of frustration later.

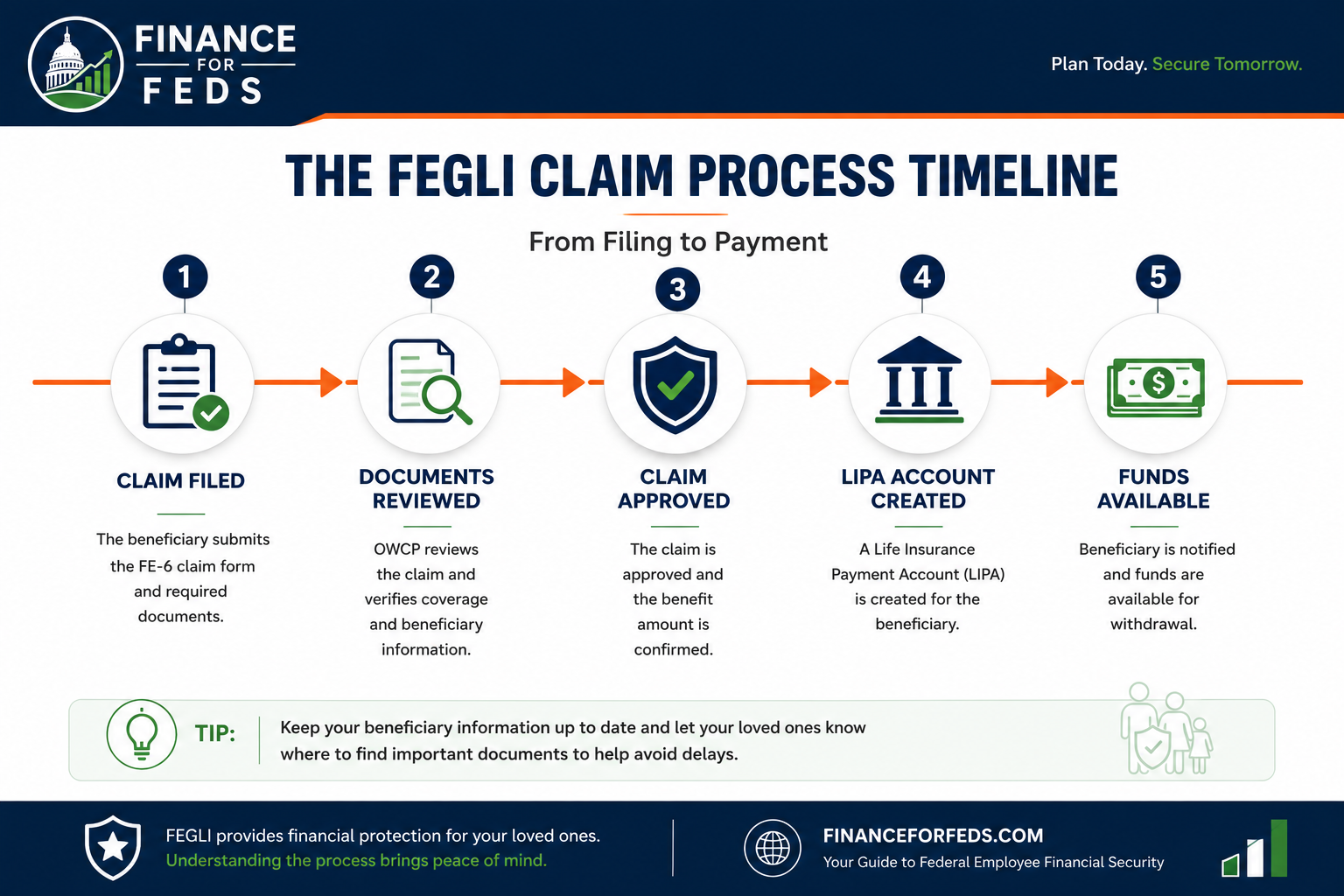

The FEGLI Claim Process Timeline

What Happens After the Claim Is Filed?

Once the claim is received, it is reviewed by the Office of Federal Employees’ Group Life Insurance.

At this stage, several things are verified:

- Coverage amount

- Beneficiary designation

- Eligibility

- Required documentation

If everything is in order, the claim moves forward. Most claims are processed without significant complications. The key factor is ensuring that all paperwork is complete and accurate from the beginning. This is one reason beneficiary designations should be reviewed periodically. An outdated designation can create delays and confusion that are entirely avoidable.

How Long Does It Take to Receive FEGLI Benefits?

One of the first questions families ask after filing a claim is: “When will the money arrive?”

The answer depends on several factors, including the completeness of the claim and whether there are any questions regarding beneficiaries. In straightforward situations, claims are often processed within a few weeks. That timeline can feel like an eternity to a grieving family, but compared to probate and estate settlement processes, FEGLI benefits are generally distributed relatively quickly. The important thing to remember is that delays are most often caused by missing documentation, outdated beneficiary forms, or disputes among potential beneficiaries.

That’s why one of the most valuable things you can do today is review your beneficiary designations and make sure they reflect your current wishes.

Who Actually Receives the Money?

Many federal employees assume their will controls where their FEGLI proceeds go. This is one of the most common misunderstandings we encounter.

Life insurance generally passes outside of your will. Instead, FEGLI follows the beneficiary designation on file. If no beneficiary designation exists, FEGLI follows a statutory order of precedence.

In simplified terms, benefits typically flow in this order:

- Designated beneficiary

- Surviving spouse

- Children

- Parents

- Executor of the estate

- Next of kin

This means that even if your will says one thing, an outdated FEGLI beneficiary designation could direct the money somewhere entirely different. We’ve spoken with federal employees who haven’t reviewed their beneficiary forms in ten or fifteen years. Marriages, divorces, births, deaths, and other major life events can dramatically change your intentions.

A five-minute review today could prevent significant problems later.

The Question Most Families Never Ask

Let’s return to Mark. Earlier, we calculated that his FEGLI Basic benefit would be approximately $137,000. At first glance, that sounds substantial. But let’s look at the broader picture.

Suppose Mark still has:

- A $190,000 mortgage

- A $15,000 car loan

- Normal monthly household expenses

If his family used the FEGLI proceeds to eliminate debt, almost the entire benefit could disappear immediately. The life insurance would still have done exactly what it was designed to do. The problem isn’t that FEGLI failed. The problem is that many federal employees mistake Basic FEGLI for a complete financial protection strategy. For some households, it may be sufficient. For many others, it is only a starting point.

Why Understanding Your Coverage Matters

One of the goals of this website is to help federal employees move beyond assumptions and start working with real numbers. Most people know their salary. Most people know their mortgage balance. Very few have ever calculated how much money their family would actually need if they were no longer there to provide income.

That calculation can be eye-opening. In some cases, families discover they are adequately protected. In others, they discover a significant coverage gap. The important thing is knowing where you stand.

Financial planning is rarely about achieving perfection. It’s about reducing uncertainty.

What Should You Do Next?

If you’ve never reviewed your FEGLI coverage, now is a good time.

Ask yourself:

- Who is listed as my beneficiary?

- How much coverage do I currently have?

- Would my family have enough income if I were gone tomorrow?

- Do I have additional coverage through FEGLI, WAEPA or private insurance?

- Have I actually calculated my family’s financial needs?

Many federal employees are surprised by the answers.

The Bottom Line

FEGLI is one of the most valuable benefits available to federal employees. It provides real protection and can deliver meaningful financial support to surviving family members. But understanding how the process works is just as important as having the coverage itself. Your family shouldn’t have to guess where to start, who to contact, or whether they’ll have enough resources to move forward.The more prepared you are today, the fewer questions they’ll have to answer tomorrow.

And perhaps the most important lesson is this:

The question isn’t whether FEGLI pays. The question is whether what it pays is enough. That’s a question every federal employee should answer long before a claim is ever filed.

Next Steps

Try the Federal Employee Life Insurance Calculator to determine:

- Your current FEGLI benefit

- Your total insurance coverage

- Your family’s estimated financial need

- Your potential coverage gap

Knowing your numbers today can help your family tomorrow.

Related Articles

- FEGLI vs WAEPA: Which Is Better for Federal Employees?

- How Much Life Insurance Do Federal Employees Actually Need?

- FEGLI Option B Explained

- Should You Keep FEGLI in Retirement?

Related Tools

Sign up for our newsletter!

Get the latest from Finance For Feds straight to your inbox.