How Much Life Insurance Do Federal Employees Actually Need? (Simple Formula + Real Examples)

If you are a federal employee, there is a good chance you already have some life insurance.

Maybe you have FEGLI Basic because it was part of your benefits package when you started. Maybe you added FEGLI Option B years ago and have not looked at it since. Maybe you picked up WAEPA coverage after hearing about it from a coworker. Or maybe you simply know that something comes out of your paycheck for life insurance, but you are not completely sure what your family would actually receive.

That is more common than people admit.

The problem is that having life insurance is not the same thing as having enough life insurance.

A federal employee can have FEGLI, WAEPA, a pension, TSP savings, and strong benefits, and still leave a surviving spouse with a major financial gap.

That does not mean every federal employee needs millions of dollars of coverage. Some do not. But it does mean the right number should be calculated, not guessed.

The goal is not to buy as much insurance as possible.

The goal is to protect the people who depend on your income.

The Problem With the “10 Times Salary” Rule

Most people have heard the old rule of thumb:

“You need 10 times your salary in life insurance.”

It is easy to remember. It is also often wrong.

For some federal employees, 10 times salary may be too much. A single employee with no dependents, no major debts, and significant savings may not need much life insurance at all.

For others, 10 times salary may not be nearly enough. A federal employee with a spouse, young children, a large mortgage, limited savings, and one primary household income may need more than a simple salary multiple suggests.

That is why the better question is not, “What rule of thumb should I use?”

The better question is, “What financial problem would my death create, and how much money would it take to solve it?”

That is where the calculation begins.

A Simple Formula That Actually Works

A practical life insurance estimate can be built with one simple formula:

Total Life Insurance Needed = Income Replacement + Debts – Existing Resources

That is it.

You estimate how much income your family would need to replace, add the debts or obligations you want paid off, and subtract the resources already available.

This approach is not perfect, but it is far better than guessing.

It also works especially well for federal employees because many of the inputs are knowable. You can estimate your FEGLI Basic amount, look at your WAEPA or other coverage, identify your debts, and decide how many years of income support your family would need.

The formula forces clarity.

And clarity is the point.

Start With Income Replacement

For most households, income replacement is the biggest part of the life insurance need.

If your paycheck disappeared tomorrow, how long would your family need support?

Some families may only need a few years because the surviving spouse earns enough, the mortgage is small, or retirement is close. Other families may need 15, 20, or 25 years of support, especially if children are young or one spouse is financially dependent on the other.

Imagine a federal employee earning $207,000 per year.

If the goal is to replace 20 years of income, the basic starting point is:

$207,000 x 20 = $4,140,000

That number can feel shocking at first.

But remember, this is not saying the family must buy exactly $4.14 million of insurance. It is simply the starting point before adjusting for other income, savings, debts, and goals.

Now assume the employee’s spouse earns $85,000 per year.

Because the spouse still has income, the household may not need to replace the full $207,000. A practical adjustment might count about 75% of the spouse’s income as available support, allowing some room for taxes, benefits, household changes, and flexibility.

That would be:

$85,000 x 75% = $63,750

Over 20 years, that spouse-income offset equals:

$63,750 x 20 = $1,275,000

So the net income replacement need becomes:

$4,140,000 – $1,275,000 = $2,865,000

That is the first major number.

The family may not need the full $4.14 million because the surviving spouse has income. But they may still need nearly $2.9 million if the goal is to preserve long-term household stability.

Add Debts and Major Obligations

The next step is to add debts.

This usually includes a mortgage, car loans, student loans, personal loans, or any other obligation you would not want your surviving spouse to carry alone.

In this example, assume the household has:

Mortgage: $190,000

Car loan: $15,000

Total debt:

$190,000 + $15,000 = $205,000

Now add that to the income replacement need:

$2,865,000 + $205,000 = $3,070,000

This means that under these assumptions, the family would need about $3.07 million before subtracting existing life insurance or other available resources.

This is where many federal employees start to realize that FEGLI Basic alone may not be enough.

Subtract Existing Coverage

Now we look at what is already in place.

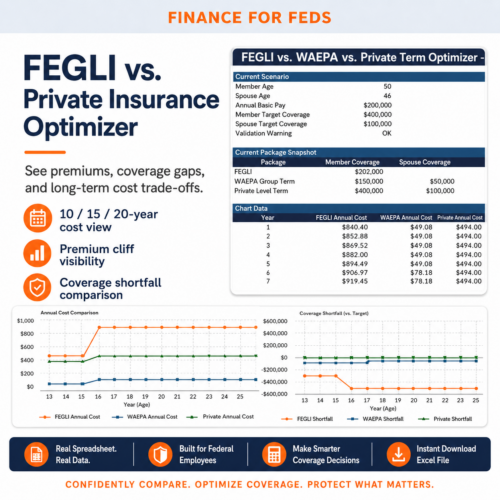

For federal employees, FEGLI Basic is often the starting point. OPM explains that FEGLI Basic generally equals your annual basic pay rounded up to the next even $1,000, plus $2,000, with a $10,000 minimum. Eligible employees are automatically enrolled in Basic unless they waive it.

For a $207,000 salary, FEGLI Basic would be approximately:

$207,000 + $2,000 = $209,000

Now assume the employee also has $150,000 of WAEPA coverage.

Existing coverage would be:

FEGLI Basic: $209,000

WAEPA: $150,000

Total existing life insurance:

$209,000 + $150,000 = $359,000

Now subtract that from the total need:

$3,070,000 – $359,000 = $2,711,000

That is the estimated coverage gap.

Again, this does not automatically mean the employee must go buy exactly $2.711 million of additional coverage. It means that if the planning goal is 20 years of income replacement, plus debt payoff, and the only existing coverage is FEGLI Basic plus $150,000 of WAEPA, the current coverage is far below the calculated need.

That is the point of the exercise.

It turns a vague feeling into a real number.

Why Federal Employees Often Underestimate the Gap

Federal employees have strong benefits, and that can create a false sense of security.

FEHB, FERS, TSP, FEGLI, sick leave, annual leave, and survivor benefits are valuable. But they do not automatically replace a full working income for a surviving spouse.

FEGLI Basic is helpful, but for many employees it is a foundation, not a complete life insurance plan. A $100,000 salary may produce roughly $102,000 of FEGLI Basic coverage. A $207,000 salary may produce roughly $209,000. Those are meaningful amounts of money, but they may not be enough to pay off a mortgage, replace income, and create long-term stability for a surviving spouse.

Optional FEGLI coverage can add more, but it needs to be reviewed carefully because optional coverage costs can rise with age. WAEPA or private term insurance may also be part of the solution, depending on health, age, underwriting, cost, and coverage needs. WAEPA states that eligible current and former civilian federal employees can apply for up to $1.5 million of group term life insurance, often with no medical exam, though additional underwriting review may be required for some applicants.

The mistake is not choosing FEGLI, WAEPA, or term insurance.

The mistake is choosing any coverage amount without first calculating the actual need.

What About the FERS Pension?

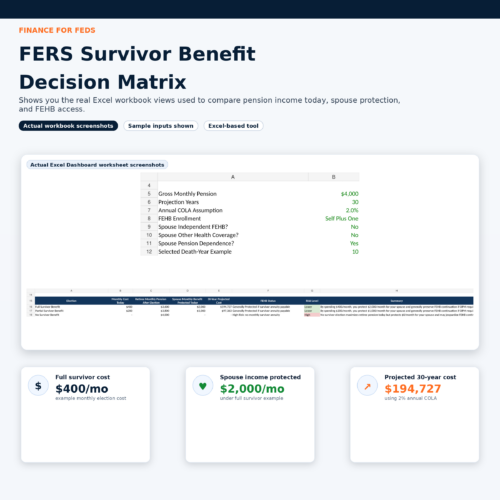

The FERS pension can help a surviving spouse, but it should not be treated as a complete life insurance substitute.

For retired federal employees, a survivor benefit can provide ongoing income to a spouse, depending on the election made at retirement. OPM states that a maximum survivor annuity provides 50% of the retiree’s unreduced annuity to the spouse, while a partial survivor annuity provides 25%; those elections reduce the retiree’s annuity by 10% or 5%, respectively.

That is valuable.

But it is not the same thing as replacing a full salary.

The survivor benefit may be only a portion of the pension. It may depend on retirement elections. It does not eliminate debts automatically. It may not solve a large income gap for a younger surviving spouse. And for an employee who dies while still working, the survivor benefit rules are different from simply receiving the employee’s full paycheck.

So yes, federal benefits matter.

But they should be included in the plan, not used as a reason to avoid planning.

Think in Terms of Risk, Not Just Replacement

Some households do not actually want or need to replace every dollar of income for 20 years.

That is fine.

Life insurance planning should match the real goal.

For one family, the goal might be full income replacement until the surviving spouse reaches retirement age.

For another, the goal might be to pay off the mortgage, eliminate debts, and provide five years of breathing room.

For another, the goal might be to cover final expenses and leave a modest cushion because there are no dependents and plenty of savings.

This is why the formula is flexible.

You can change the years of income replacement. You can decide whether to include the mortgage. You can subtract savings, TSP, brokerage accounts, or other assets if you are comfortable using those resources. You can include college costs or leave them out. You can account for spouse income or assume none.

The right answer depends on what you want the insurance to accomplish.

A More Practical Way to Frame the Decision

Instead of asking, “How much life insurance should I have?” ask:

“What would I want my spouse or family to be able to do if I died?”

Maybe the answer is:

Stay in the house.

Pay off the mortgage.

Avoid selling investments during a crisis.

Replace income for 10 to 20 years.

Cover childcare or eldercare.

Delay major decisions for a year or two.

Retire on schedule.

Avoid financial panic.

That list is more useful than a generic salary multiple.

Life insurance is not really about death. It is about buying time, flexibility, and choices for the people left behind.

How FEGLI Fits Into the Plan

FEGLI Basic is often worth viewing as the first layer of protection.

It is easy to understand, connected to federal employment, and automatic for many eligible employees unless waived. It can provide an immediate foundation of coverage without requiring the employee to shop for a separate policy.

But Basic coverage is usually not designed to solve every family need.

That is why many federal employees eventually consider supplemental protection. That may include FEGLI Option B, WAEPA, or private term life insurance.

The best strategy for many households is not necessarily to replace one with another. It may be to keep FEGLI Basic and add enough supplemental coverage to close the actual gap.

That approach gives the family a baseline benefit while using additional coverage to handle the bigger planning need.

Do Not Forget Existing Resources

Existing resources can reduce the amount of insurance needed.

This might include emergency savings, brokerage accounts, Roth IRA assets, other life insurance, home equity, or money the surviving spouse could reasonably use.

But be careful with retirement accounts.

A TSP balance may be available to beneficiaries, but that does not always mean it should be treated as a direct substitute for life insurance. If the surviving spouse needs that money for their own retirement later, using it immediately to replace lost income may create a different problem down the road.

The same is true for the house.

Home equity is real wealth, but a surviving spouse may not want to sell the home immediately after a death. Counting home equity as a life insurance replacement only works if selling or borrowing against the home is actually part of the plan.

This is why liquidity matters.

Life insurance creates cash at the moment the family may need it most.

A Simple Target Range

For many federal employees with spouses, children, mortgages, or one primary household income, total life insurance needs can easily land in the $1 million to $3 million range.

But that range is not a rule.

Dual-income households with no children and manageable debts may need less.

Single-income households with young children may need more.

Employees close to retirement may need less income replacement than employees in their thirties or forties.

Employees with large mortgages, dependent parents, or limited savings may need more protection.

The formula matters more than the range.

The Bottom Line

There is no universal right amount of life insurance for federal employees.

The right amount depends on your income, your debts, your spouse’s income, your savings, your dependents, your retirement timeline, and what you want the insurance to accomplish.

A simple formula can bring order to the decision:

Total Life Insurance Needed = Income Replacement + Debts – Existing Resources

In the example above, a federal employee earning $207,000 with a spouse earning $85,000, a $190,000 mortgage, a $15,000 car loan, FEGLI Basic of about $209,000, and WAEPA coverage of $150,000 could still have an estimated coverage gap of about $2.711 million if the goal is 20 years of income replacement.

That does not mean everyone needs that much coverage.

It means guessing is dangerous.

FEGLI Basic can be a useful foundation. WAEPA or term insurance can help fill a gap. The FERS pension and survivor benefits can help, but they are not a full replacement for a working income.

The real goal is not to own a certain type of policy.

The real goal is to make sure your family would have enough cash, income, and flexibility to move forward if the unexpected happened tomorrow.

Related Tools

Sign up for our newsletter!

Get the latest from Finance For Feds straight to your inbox.