FEGLI vs WAEPA: Which Life Insurance Is Better for Federal Employees?

Every year, thousands of federal employees ask some version of the same question:

“Should I keep FEGLI or switch to WAEPA?”

At first, it sounds like a simple comparison. Two life insurance options. Two sets of premiums. One decision. But for most federal employees, the answer is not as simple as picking the cheaper policy. The real mistake is assuming this has to be an either-or decision.

FEGLI and WAEPA solve different problems. FEGLI is convenient, familiar, and often easy to keep because it is built directly into the federal benefits system. WAEPA may offer more flexible coverage amounts and, for some healthy applicants, potentially lower long-term costs. But those advantages come with a different kind of tradeoff.

To see why, let’s start with Sarah.

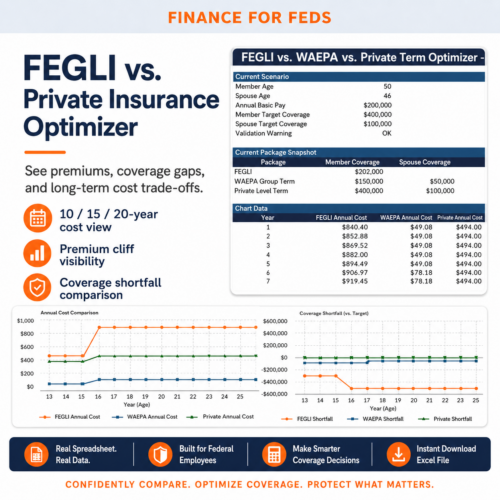

Sarah is a 49-year-old GS-13 manager with more than twenty years of federal service. She has carried FEGLI Basic for most of her career and has never thought much about it. The premium comes out of her paycheck, the coverage is there, and it feels like one of those benefits she is supposed to keep.

Then she attends a retirement seminar. Someone mentions WAEPA. A presenter says it may be cheaper. A coworker tells her FEGLI is overpriced. Another coworker says FEGLI is safer because it is connected to federal employment. By the end of the week, Sarah is more confused than when she started. That is exactly where many federal employees end up. They hear opinions before they understand the structure. And with life insurance, structure matters.

What FEGLI Really Is

FEGLI stands for Federal Employees’ Group Life Insurance.

For many federal employees, it is the first life insurance coverage they ever have. Eligible employees are generally automatically enrolled in Basic coverage unless they waive it. Basic coverage is calculated as the greater of your annual basic pay rounded up to the next even $1,000 plus $2,000, or $10,000. The government generally pays one-third of the Basic premium and the employee pays two-thirds, with a separate rule for Postal employees.

That automatic, payroll-based setup is one of FEGLI’s biggest strengths.You do not have to shop for a policy. You do not have to compare dozens of companies. Basic coverage does not require the kind of underwriting process many people associate with private life insurance. It is simple, familiar, and tied directly to your federal employment.

FEGLI also offers optional coverage. Option A provides $10,000 of additional coverage. Option B allows you to elect one to five multiples of your annual basic pay rounded up to the next even $1,000. Option C provides family coverage for a spouse and eligible dependent children.

But there is a catch. FEGLI Basic and FEGLI Optional coverage are priced very differently.

Basic coverage uses a level premium structure, meaning the employee rate for Basic coverage does not change just because you get older, although the overall rate structure can be adjusted. OPM explains that younger employees pay the same Basic rate as older enrollees, regardless of age or health status.

Optional coverage is where many federal employees start to feel the squeeze.

Option B, in particular, can become expensive as you age. OPM’s employee premium table shows Option B rates rising by age band. For example, the monthly cost per $1,000 of Option B coverage is listed as $0.217 for ages 50–54, $0.390 for ages 55–59, $0.867 for ages 60–64, and continues higher at older ages.

This is why FEGLI can feel inexpensive early in a career and surprisingly expensive later.

FEGLI is not bad. But it must be understood.

What WAEPA Really Is

WAEPA stands for Worldwide Assurance for Employees of Public Agencies.

It is a nonprofit organization that offers group term life insurance for current and former civilian federal employees. WAEPA states that its group term life insurance is available to current and former civilian federal employees under age 70. Unlike FEGLI, WAEPA is not automatically part of your federal benefits package. You apply separately. WAEPA states that applicants may apply for up to $1.5 million in group term life insurance, often with no medical exam required, though some applicants may need additional underwriting review, medical records, or a medical exam.

That difference is important.

FEGLI is built around access and simplicity. WAEPA is built more like an alternative or supplemental insurance option for federal employees who want to compare coverage and cost.

WAEPA’s rates are also age-banded. WAEPA states that premiums are based on age and increase when you enter a new five-year age group. It also says coverage can carry with you up to your 85th birthday, with maximum coverage beginning to reduce at age 60. So WAEPA is not “level forever” insurance. It is still term life insurance with changing costs over time.

But depending on your age, health, coverage amount, and family needs, it may be worth comparing against FEGLI, especially if you are carrying expensive FEGLI Option B coverage.

The Cost Question Everyone Asks

When Sarah first compares FEGLI and WAEPA, she does what most people do. She looks at today’s premium. That is understandable, but it is also incomplete.

The better question is not, “What is cheaper this paycheck?” The better question is, “What will this coverage cost me over the next 10, 15, or 20 years?”

That is where the FEGLI conversation often changes. A federal employee in their thirties may barely notice Option B premiums. But by the fifties and sixties, the cost can become much more meaningful, especially for employees carrying multiple salary multiples.

Imagine someone with a $200,000 salary who carries five multiples of Option B.

That could create roughly $1,000,000 of Option B coverage, because Option B is based on multiples of salary rounded up to the next even $1,000. At age 50, the cost may be manageable for some households. But as the employee enters later age bands, the same coverage can become dramatically more expensive.

This does not mean everyone should cancel FEGLI Option B. It means everyone should project it. A life insurance decision that looks fine at 49 may look very different at 59.

When FEGLI May Be the Better Choice

FEGLI can be the better choice when access matters more than price. This is especially true for employees with health issues. A healthy employee may underestimate how valuable guaranteed or easily accessible coverage can be. But someone who has been declined for private insurance, rated up due to health conditions, or delayed because of underwriting knows that access is not a small detail. Coverage you can actually get may be more valuable than coverage that looks cheaper on a quote sheet.

FEGLI may also make sense for employees who value simplicity. There is a real benefit to having life insurance integrated into your federal benefits package. Premiums are handled through payroll. Coverage is familiar. Beneficiary forms and federal benefits processes are part of a system many employees already understand.

And for employees close to retirement, switching coverage should be approached carefully.

FEGLI can be continued into retirement if you meet specific requirements, including being entitled to retire on an immediate annuity, being insured for the required five-year period before the annuity begins or for all opportunities if less than five years, being enrolled on the date of retirement, and not converting to an individual policy. That does not automatically mean FEGLI is the best retirement solution. It simply means the retirement rules matter.

For Sarah, who is 49 and thinking seriously about retirement, the decision is not just about today’s premium. It is about what coverage she can keep, what it will cost later, and what her family would actually need if she died before or during retirement.

When WAEPA May Make More Sense

WAEPA often deserves a serious look when a federal employee is healthy, needs more coverage, and wants to compare long-term cost.

For example, a younger or mid-career employee with a spouse, children, a mortgage, and a large income-replacement need may discover that FEGLI Basic alone is nowhere near enough. FEGLI Basic is tied to salary. WAEPA allows eligible members to apply for coverage amounts that are not capped by salary in the same way. WAEPA states that eligible members can apply for up to $1.5 million in group term life insurance. That flexibility can matter.

A federal employee earning $100,000 with young children may need far more than roughly $102,000 of FEGLI Basic coverage. A federal employee earning $200,000 with a large mortgage and dependents may also find that Basic coverage alone does not come close to replacing income.

WAEPA can be attractive because it allows the employee to choose a coverage amount based on family need, not just federal salary formulas. But the key phrase is “if you qualify.”

WAEPA may involve health questions and underwriting. Many applicants may receive quick decisions, but WAEPA also notes that some applications require additional review, which may involve more information, medical records, or a medical exam. That is the tradeoff.

FEGLI is easier to access. WAEPA may be more customizable. Neither is automatically better.

The Real Problem Is Usually Underinsurance

A lot of federal employees spend too much time debating FEGLI versus WAEPA and not enough time asking a more important question: “How much life insurance does my family actually need?”

That is the missing step. Before comparing premiums, you need to understand the job the insurance is supposed to do. Is it supposed to pay off a mortgage? Replace income for a spouse? Fund college for children? Cover final expenses? Give a surviving spouse time to adjust? Protect a family from selling a home during a crisis? A policy is only “good” if it solves the right problem.

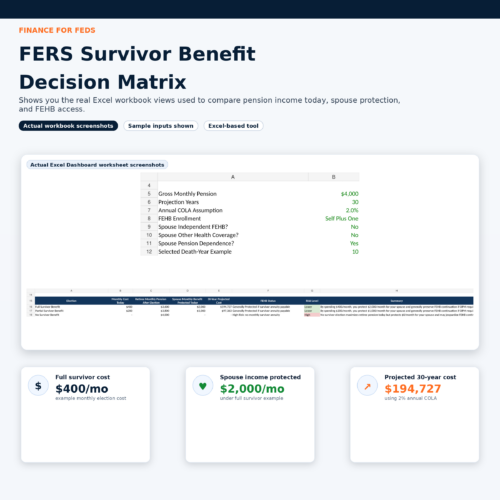

Consider a federal employee earning $200,000 annually with a spouse, two children, and a $250,000 mortgage.

Their FEGLI Basic coverage might be approximately $202,000. At first glance, that sounds like a lot of money. But if the family uses the benefit to pay off the $250,000 mortgage, the entire FEGLI Basic benefit is gone and still does not fully eliminate the debt.

That leaves nothing for income replacement. Nothing for childcare support. Nothing for college planning. Nothing for the surviving spouse’s long-term financial security.

In that case, the issue is not that FEGLI failed. FEGLI Basic did exactly what it was designed to do. The issue is that the family’s need was bigger than the Basic benefit.

That is where supplemental coverage enters the conversation. It might be FEGLI Option B. It might be WAEPA. It might be a private term policy. It might be a combination.

But the starting point is the coverage need, not the product name.

Why a Combination Strategy Often Works

The most practical answer for many federal employees is not “FEGLI or WAEPA.” It is “FEGLI plus something else.”

For example, an employee may decide to keep FEGLI Basic because it is simple, familiar, and connected to federal benefits. Then they may add WAEPA coverage to fill a larger income-replacement gap. That approach can create a better balance.

FEGLI Basic provides a baseline. WAEPA or another policy provides additional coverage. The employee avoids relying entirely on one program while also avoiding the mistake of assuming Basic coverage is enough. This is often where the conversation becomes more productive. Instead of asking, “Which one wins?” the employee asks, “What combination gives my family the right amount of protection at a reasonable cost?”

That is a much better question.

A Better Framework for Deciding

For Sarah, the answer starts to become clearer when she stops listening to coworkers and starts looking at her own numbers.

She looks at her age, her health, her spouse’s income, and at the mortgage. Sarah then considers how long her family would need income support. She reviews what coverage she already has and what it would cost to keep it. Only then does the FEGLI versus WAEPA decision become useful.

Here is a practical way to think about it.

FEGLI may be a better fit if health concerns make underwriting difficult, simplicity is a priority, you are comfortable with the coverage amount, or you are close to retirement and want to be careful before changing existing benefits.

WAEPA may be worth considering if you are healthy, need more coverage than FEGLI Basic provides, want to compare long-term premium costs, or want coverage that is not limited by the same salary-based formula as FEGLI.

A combination may make sense if you want to keep guaranteed baseline protection through FEGLI Basic while adding more coverage through WAEPA or another policy. The right answer depends on the household.

A single employee with no dependents and significant savings may not need much life insurance at all.

An employee who is married with young children, a large mortgage, and one primary income may need far more than FEGLI Basic.

A federal employee near retirement may care less about replacing twenty years of income and more about protecting a spouse, covering debts, or leaving enough liquidity to avoid a financial scramble.

The product decision follows the planning decision.

Do Not Cancel Coverage Before the Replacement Is Active

There is one rule that deserves special attention: Do not cancel or reduce existing life insurance until replacement coverage is fully approved, active, and understood.

This is especially important if you are applying for WAEPA or private coverage and currently have FEGLI Option B.

A quote is not the same thing as approved coverage. An application is not the same thing as active coverage. A preliminary estimate is not a guarantee.

If you are replacing coverage, wait until the new policy is actually in force before making changes to existing protection. Otherwise, you could accidentally create a coverage gap at exactly the wrong time.

The Bottom Line

FEGLI and WAEPA are not enemies. They are tools.

FEGLI is often strongest when you value simplicity, accessibility, and integration with federal benefits. WAEPA may be attractive when you are healthy, need more coverage, and want to compare long-term costs.

For some federal employees, FEGLI alone is enough. For others, WAEPA may provide valuable supplemental protection.

Often, the most thoughtful answer for many is a combination: keep FEGLI Basic and use WAEPA or another policy to fill the gap.

But before choosing either one, answer the most important question first: “How much life insurance does my family actually need?” Until you know that number, it is impossible to know whether FEGLI, WAEPA, or any other policy is truly enough.

The goal is not to win a debate about which program is better. The goal is to make sure your family would be financially secure if the unexpected happened tomorrow.

Related Articles

- What Happens to Your FEGLI When You Die?

- How Much Life Insurance Do Federal Employees Actually Need?

- FEGLI Option B Explained

- Should You Keep FEGLI in Retirement?

Related Tools

Sign up for our newsletter!

Get the latest from Finance For Feds straight to your inbox.