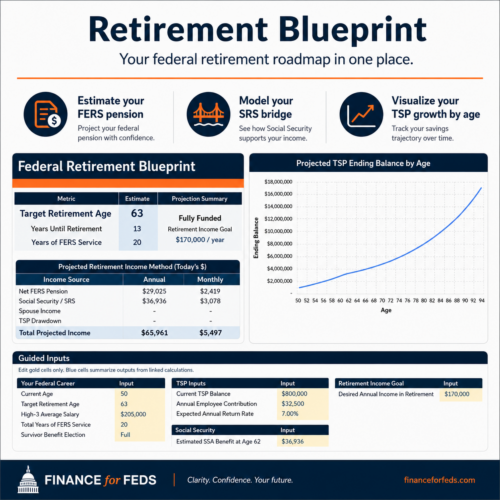

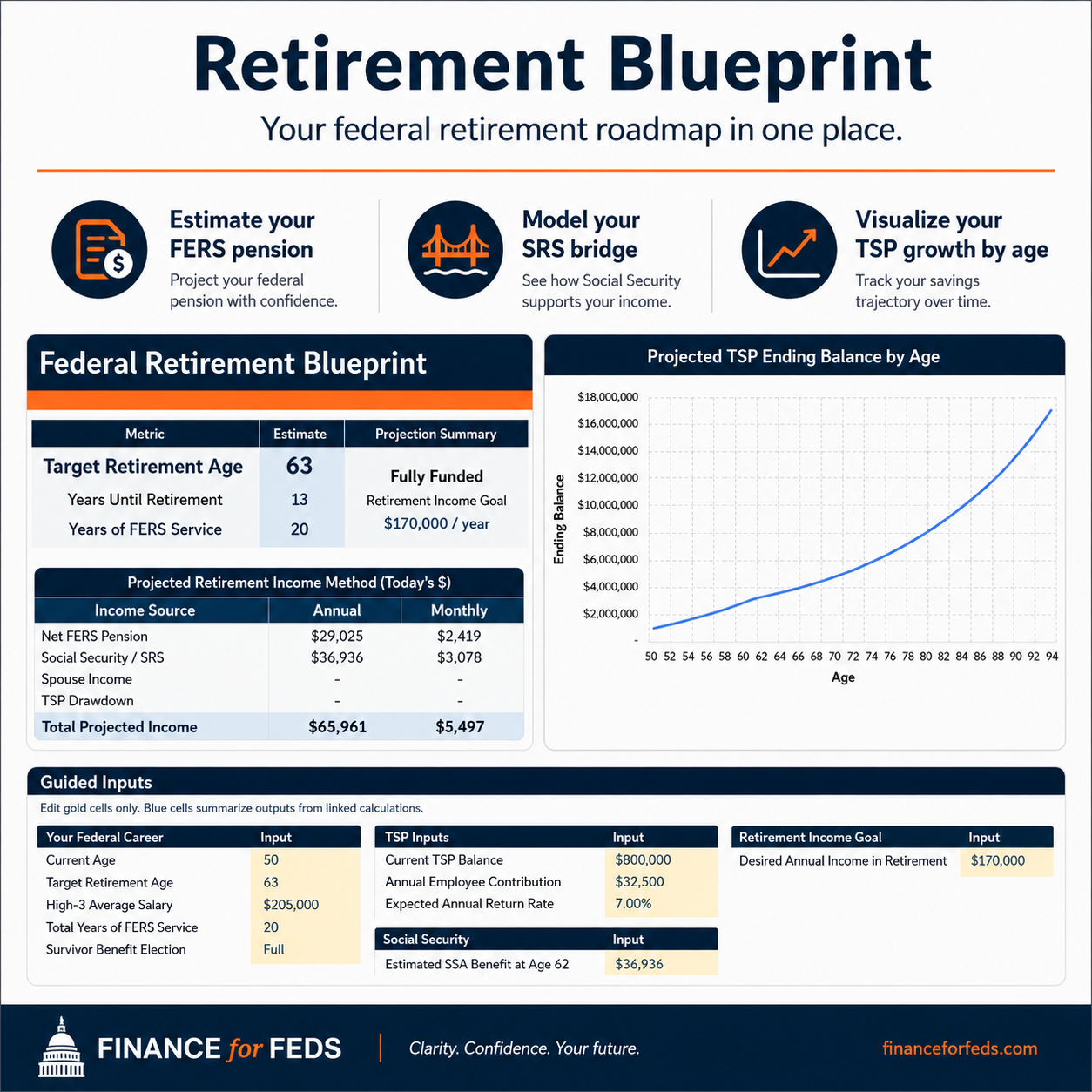

How the FERS Pension Is Calculated: Formula and Real Examples

Imagine sitting down to plan the final chapter of a dedicated, 25-year career in the federal government. For decades, you’ve watched a small portion of every paycheck disappear into the Federal Employees Retirement System (FERS). You know it’s building a financial bedrock for your future, but what does that bedrock actually look like when the regular paychecks stop?

To see how the math translates into real life, it helps to imagine walking through the final years of your career. The FERS formula itself relies on three interconnected pieces: your peak earnings, your total time on the job, and a small percentage called the multiplier.

The journey to your final number starts with your “High-3.” This isn’t just your final salary; it’s the exact average of your highest three consecutive years of basic pay, which usually happens right at the finish line of your career. Imagine that during your final three years, your salary climbs steadily from $195,000, to $205,000, and finally peaks at $210,000. When you average those three highest consecutive years together, you establish a baseline figure of about $203,000.

Next, you look at the clock to calculate your total Years of Service. Every year of full-time federal service—along with any eligible military time you’ve chosen to buy back—adds weight to your future pension. For this milestone, let’s say your career spans exactly 25 years.

Finally, you encounter the multiplier, a small decimal that acts as the gatekeeper to your final total. For most federal workers, this multiplier sits at a standard 1%. If you choose to retire before age 62, the math flows cleanly: you multiply your $203,000 High-3 by your 25 years of service, and then apply that 1% standard multiplier. The result is a guaranteed, predictable $50,750 per year.

Let’s calculate:

- High-3: $203,000

- Years: 25

- Multiplier: 1%

Pension = $203,000 × 25 × 1% = $50,750 per year

However, there is a massive incentive hidden in the timing of your departure. If you can hang onto your badge until you turn 62, the rules change entirely in your favor. Because you have achieved more than 20 years of service and reached that magic age, your multiplier automatically bumps up to 1.1%. It sounds like a tiny shift, but when applied to that same $203,000 baseline and 25 years of service, your annual pension jumps to $55,825. That is an extra $5,075 landing in your pocket every single year, simply because you timed your exit strategically.

Same example:

= $203,000 × 25 × 1.1% = $55,825 per year

In the real world, this FERS pension is an incredible asset. Unlike private-sector retirement accounts that swing violently with the stock market, this income is entirely guaranteed. Even better, once you retire, it adjusts for inflation, ensuring your buying power doesn’t erode over time. It gives you the peace of mind to invest your other savings more confidently, knowing your basic needs are covered.

Yet, a dangerous trap many federal employees fall into is assuming this pension will fully replace their working income. In reality, a FERS pension typically only replaces about 25% to 40% of what you were making. In our scenario, even with the age 62 bonus, a $55,825 pension is a far cry from the $210,000 salary you were used to earning.

Ultimately, the FERS pension isn’t a complete retirement plan on its own—it is an unbreakable foundation. To maintain your lifestyle and protect your hard work, you have to actively bridge that remaining 60% to 75% gap using your Thrift Savings Plan (TSP) and Social Security. Knowing your exact pension number ahead of time gives you the power to plan for that gap long before you ever sign your final retirement papers.

Bottom Line

- FERS is a powerful foundation

- But it’s only one piece of your retirement plan

- Understanding your number is critical

Want to explore strategies for bridging that remaining income gap with your TSP?

Related Tools

Sign up for our newsletter!

Get the latest from Finance For Feds straight to your inbox.