Can I Retire at 57 as a Federal Employee? (What You Need to Know)

For many federal employees, age 57 has a special pull.

It is the age that gets circled quietly in the back of the mind. It shows up in retirement calculators, HR conversations, financial planning spreadsheets, and hallway conversations with coworkers who are counting down the years.

“Can I retire at 57?”

The answer is: maybe.

For some federal employees, 57 is the doorway to a full immediate FERS retirement. For others, it is only the first age where retirement becomes possible, but not necessarily painless. And for some, retiring at 57 could mean giving up benefits, taking a permanent pension reduction, or creating a health insurance gap that is more expensive than expected.

So age 57 matters.

But it is not magic by itself.

Under FERS, your retirement eligibility depends on three things working together: your age, your years of creditable service, and the type of retirement you are actually eligible to claim. OPM lists several voluntary immediate retirement combinations, including age 62 with 5 years, age 60 with 20 years, Minimum Retirement Age with 30 years, and Minimum Retirement Age with at least 10 years, subject to reduction rules for MRA+10 retirements (OPM FERS Eligibility).

That means the real question is not simply, “Can I retire at 57?”

The better question is, “What kind of retirement can I take at 57, and what would I be giving up?”

Why Age 57 Matters

For federal employees born in 1970 or later, the Minimum Retirement Age, commonly called MRA, is 57. Employees born earlier may have a lower MRA, based on OPM’s birth-year table (OPM FERS Eligibility).

Your MRA is important because it is the earliest age at which many regular FERS employees can retire voluntarily under standard rules.

But reaching your MRA does not automatically mean you can retire with a full, unreduced pension.

That is where years of service come in.

If you reach your MRA and have 30 years of creditable service, you can generally retire on an immediate, unreduced FERS pension. That is the clean version of retiring at 57.

If you reach 57 with only 10 to 29 years of service, you may still have options, but the decision gets more complicated.

The Cleanest Path: Age 57 With 30 Years

Let’s start with the version most people have in mind.

Sarah is a federal employee born after 1969, so her MRA is 57. She started federal service at 27 and will have 30 years of creditable service by the time she turns 57.

For Sarah, age 57 is not just symbolic. It is a real eligibility point.

Because she has reached her MRA and has 30 years of service, she can generally retire under the MRA+30 rule with an immediate, unreduced FERS annuity. OPM lists MRA with 30 years as one of the combinations for voluntary immediate retirement with no age reduction (OPM Types of Retirement).

Now let’s put numbers to it.

Assume Sarah’s high-3 average salary is $100,000 and she has exactly 30 years of creditable service.

The basic FERS pension formula for most regular employees retiring before age 62 is:

High-3 salary x 1% x years of service

So Sarah’s estimated annual pension would be:

$100,000 x 1% x 30 = $30,000 per year

That equals about:

$2,500 per month before taxes, survivor benefit reductions, FEHB premiums, and other deductions

That is not her full retirement income. It is one piece of the retirement puzzle.

She may also have TSP savings. She may eventually claim Social Security. If she qualifies, she may receive the FERS Special Retirement Supplement until age 62. But the FERS pension itself would begin right away and would not be reduced simply because she retired at 57.

This is the version of “retire at 57” that many federal employees are aiming for.

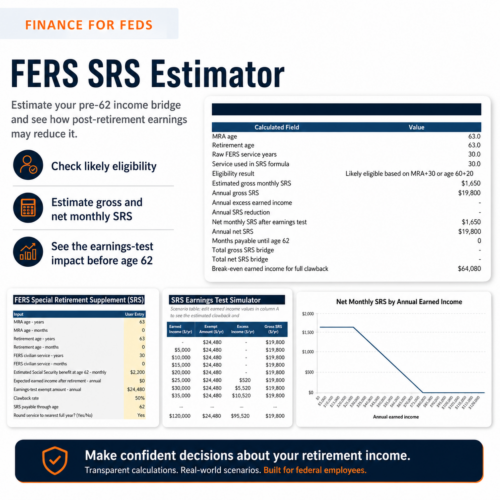

The FERS Special Retirement Supplement

One of the biggest reasons MRA+30 retirement can be powerful is the FERS Special Retirement Supplement, often shortened to SRS.

The supplement is designed to act as a bridge between retirement and age 62, when Social Security first becomes available. It is not exactly Social Security, and it is not calculated by the Social Security Administration, but it is meant to approximate the portion of your age-62 Social Security benefit earned during your FERS civilian service.

A common rough estimate is:

Age-62 Social Security estimate x years of FERS service / 40

For example, assume Sarah’s estimated Social Security benefit at age 62 is $2,200 per month and she retires at 57 with 30 years of FERS service.

Her rough SRS estimate would be:

$2,200 x 30 / 40 = $1,650 per month

That could be a major part of her retirement bridge from 57 to 62.

But there are two important cautions.

First, the supplement generally stops at age 62, whether or not you actually claim Social Security at 62.

Second, the supplement can be reduced if you have earned income above the annual earnings-test limit. Wages and self-employment income can matter here. Pension income, TSP withdrawals, and investment income generally are not treated the same way for this purpose.

So if Sarah retires at 57 and then takes a private-sector job, she needs to understand how that income could reduce or eliminate the supplement.

Age 57 With 20 Years: Possible, But Different

Now let’s look at Mark. Mark is also 57, but he has 20 years of creditable federal service, not 30.

He has reached his MRA, so he may be eligible for an MRA+10 retirement. But if he starts his pension immediately at 57, the pension is generally reduced by 5% per year for each year he is under age 62. OPM describes this as a 5/12 of 1% reduction for each month the annuity starts before age 62 (OPM Retirement FAQs).

At 57, Mark is five years under 62.

That means the reduction could be about:

5 years x 5% = 25%

That is permanent.

If Mark’s unreduced FERS pension would have been $20,000 per year, a 25% reduction would bring it down to about $15,000 per year. That is a big trade-off.

But Mark may have another option: postpone the start of his annuity. OPM explains that under MRA+10, delaying the annuity start date can reduce or avoid the age reduction. In the special case where someone has at least 20 years of service and starts the annuity at age 60, the age reduction can be eliminated (OPM MRA+10 Postponement FAQ).

So Mark could leave federal service at 57, postpone the pension until 60, and avoid the age reduction.

But that creates another question: what does he live on between 57 and 60?

That is where retirement planning becomes real. A postponed pension may protect the monthly annuity amount, but it does not create cash flow during the waiting period. Mark would need savings, spouse income, TSP access, part-time work, or another bridge strategy.

Age 57 With 10 Years: The MRA+10 Trade-Off

Now imagine Alex. Alex reaches age 57 with 10 years of federal service. That is enough to qualify for MRA+10 retirement, but it is not enough for an unreduced immediate pension.

Alex has a choice. He could start the pension immediately at 57 and accept the permanent age reduction. Since he is five years under 62, the reduction could be about 25%. Or he could postpone the start of the pension to reduce or avoid the reduction.

If Alex waits until 62, the age reduction can generally be avoided. But again, the pension does not pay during the waiting period.

For someone with 10 years of service, retiring at 57 may be technically possible, but it may not be financially comfortable unless there are other income sources. This is why “eligible” and “ready” are not the same thing.

The FEHB Issue Can Be the Deciding Factor

For many federal employees, the biggest retirement asset is not the pension. It is FEHB.

Being able to carry Federal Employees Health Benefits into retirement can be enormously valuable, especially for someone retiring before Medicare eligibility. But the rules matter.

In general, to continue FEHB into retirement, you must retire on an immediate annuity and have been covered under FEHB, TRICARE, or CHAMPVA for the required five-year period immediately before retirement, or since your first opportunity to enroll if shorter (OPM Planning and Applying).

MRA+10 postponed retirement has a special wrinkle. If you postpone your annuity, your FEHB coverage does not simply continue as normal during the postponed period. OPM says health benefits may be temporarily continued for 18 months through Temporary Continuation of Coverage, but you generally pay the full premium plus an administrative charge. When the postponed annuity begins, if you are otherwise eligible, you can reenroll in FEHB and the government share resumes (OPM MRA+10 Postponement FAQ).

That distinction matters.

If Mark leaves at 57 and postpones his pension until 60, he may be able to restart FEHB at 60 if he meets the rules. But he still has to solve the health insurance gap from 57 to 60. That gap can be expensive. For some households, this one issue changes the entire retirement decision.

Deferred Retirement Is Not the Same as Postponed Retirement

This is one of the most confusing parts of FERS planning.

Deferred and postponed retirement sound similar in normal English, but under FERS they are not the same thing.

A postponed retirement generally applies when you are eligible for an immediate MRA+10 retirement but choose to delay the start of the annuity to reduce or avoid the age reduction.

A deferred retirement generally applies when you leave federal service before you are eligible for an immediate retirement and later claim the pension when you meet the age requirement.

The difference can be huge.

OPM states that deferred retirees are not eligible to reenroll in health benefits, life insurance, or dental and vision benefits, and they are not eligible for the FERS annuity supplement (OPM Types of Retirement). So if someone leaves federal service before reaching MRA, even with many years of service, they may eventually receive a pension, but they may lose access to FEHB in retirement.

That is why leaving at 56 with 30 years of service can be very different from leaving at 57 with 30 years of service. One year can change the category. And the category can change the benefits.

The Real Retirement-at-57 Checklist

If you are thinking about retiring at 57, do not start with your age.

Start with these questions:

- What is my exact Minimum Retirement Age?

- How many years and months of creditable service will I have?

- Am I eligible for MRA+30, MRA+10, age 60+20, or something else?

- Will my annuity be immediate, postponed, or deferred?

- Will my pension be reduced?

- Will I qualify for the FERS Special Retirement Supplement?

- Can I keep or later restart FEHB?

- How will I cover health insurance before Medicare?

- What will I live on before Social Security?

- How much do I need from TSP, savings, spouse income, or part-time work?

- Have I confirmed my service history, sick leave, military deposits, and beneficiary elections?

This is where many federal employees discover that the retirement decision is not one decision. It is a sequence of linked decisions.

The pension affects cash flow. Cash flow affects TSP withdrawals. TSP withdrawals affect taxes. Health insurance affects monthly expenses. Part-time work can affect the SRS. Survivor benefit choices affect the pension amount and spouse protection.

Age 57 is only the starting point.

So, Can You Retire at 57?

Yes, if you meet the right conditions.

If you are at your MRA and have 30 years of service, retiring at 57 can be a strong and clean FERS retirement path. You may be eligible for an immediate unreduced pension, continued FEHB if you meet the health coverage rules, and potentially the FERS Special Retirement Supplement until age 62.

If you are 57 with at least 10 but fewer than 30 years of service, you may still be able to retire under MRA+10, but you need to understand the age reduction and whether postponing the annuity makes sense.

If you are 57 with 20 years of service, postponing to age 60 may eliminate the pension reduction, but you still need a plan for income and health insurance during the gap.

If you leave before your MRA, be very careful. That may push you into deferred retirement territory, which can mean no FEHB in retirement and no FERS supplement.

The bottom line is simple:

Age 57 can be the beginning of retirement eligibility. But whether it is the right retirement age depends on your service, your benefits, your cash flow, and your ability to bridge the years before Social Security and Medicare.

For federal employees, the goal is not just to retire early. The goal is to retire early without accidentally giving up benefits that may be worth tens or even hundreds of thousands of dollars over a lifetime.

Related Tools

Sign up for our newsletter!

Get the latest from Finance For Feds straight to your inbox.